Table of Contents

Role of Technology in Personal Finance Management

Role of Technology in Personal Finance Management: Managing money used to mean balancing a checkbook by hand, storing receipts in drawers, and visiting the bank every time you needed an update on your account. Today, things look entirely different. Technology has transformed personal finance into something more accessible, transparent, and efficient. From budgeting apps and online banking to AI-driven investment platforms, digital tools are helping people make smarter decisions with their money.

This article explores the role of technology in personal finance management, how it impacts everyday financial habits, its advantages and drawbacks, and what the future may hold for money management in the digital age.

The Shift Toward Digital Finance

Personal finance management has always been about one thing: understanding where your money comes from, where it goes, and how to make it work for you. But the methods have changed dramatically.

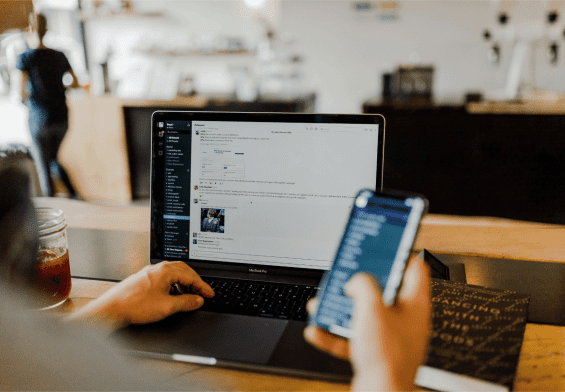

In the past, financial planning often required hiring advisors, accountants, or using pen-and-paper spreadsheets. Today, technology gives you the power to manage most aspects of your finances from the palm of your hand.

Mobile banking apps notify you when money leaves your account. Budgeting tools categorize your spending automatically. Investment platforms can rebalance your portfolio without you lifting a finger. This shift from manual to automated, from reactive to proactive, has made financial management less intimidating and more accessible.

Online Banking: The Foundation of Digital Finance

The cornerstone of personal finance technology is online and mobile banking. Nearly every financial institution now offers digital banking services, and for good reason.

- 24/7 Access: You can check your balance, transfer money, or pay bills anytime.

- Transaction Tracking: Real-time updates help you avoid overdrafts or missed payments.

- Ease of Use: Instead of long lines at the bank, a few taps on your smartphone gets the job done.

For many, mobile banking apps serve as the primary hub for financial activity. They connect to budgeting tools, payment apps, and even credit monitoring platforms, making them essential to personal finance management.

Budgeting Apps: Taking Control of Spending

One of the biggest struggles people face is understanding where their money goes. Budgeting apps like Mint, YNAB (You Need A Budget), or PocketGuard have revolutionized how individuals track spending.

These apps connect directly to your bank account and credit cards. Transactions are categorized automatically—groceries, dining out, entertainment, bills—so you see exactly where your money is flowing.

- Spending Insights: Pie charts and graphs simplify your habits visually.

- Savings Goals: Set aside money for vacations, emergencies, or big purchases.

- Accountability: Notifications and alerts help you stay within budget.

By turning raw data into actionable insights, budgeting apps empower people to make conscious decisions about their spending and saving.

Digital Payment Platforms

Cash is no longer king. Payment apps like PayPal, Venmo, and Google Pay have made digital transactions a daily norm. These tools play a huge role in personal finance by speeding up transactions, improving convenience, and reducing dependency on physical currency.

For personal finance, this has multiple benefits:

- Transparency: Every payment leaves a digital trail, making tracking easier.

- Speed: Instant transfers reduce delays in managing bills or splitting costs.

- Integration: Many apps link directly to your budget, automatically recording expenses.

However, the ease of spending can also make overspending a risk, which is why financial awareness is crucial when using these platforms.

Investment and Wealth Management Apps

Investing used to feel like something reserved for the wealthy or the financially savvy. Technology has broken down these barriers. Robo-advisors such as Betterment or Wealthfront, and trading platforms like Robinhood or eToro, make investing as simple as downloading an app.

- Accessibility: Start investing with as little as $5.

- Automation: Robo-advisors create portfolios and rebalance them automatically.

- Education: Many apps offer tutorials and resources to help beginners.

This democratization of investing has encouraged millions to start building wealth earlier than previous generations.

Credit Monitoring and Debt Management

Understanding your credit score is critical for major financial goals like buying a home or car. Technology has made credit monitoring easier than ever.

Apps like Credit Karma and Experian allow users to:

- Track credit scores in real time.

- Receive alerts for suspicious activity.

- Learn how to improve their credit health.

Similarly, debt repayment apps like Undebt.it or Debt Payoff Planner help people create strategies to eliminate debt systematically, offering motivation through progress tracking and reminders.

Artificial Intelligence in Personal Finance

One of the most exciting technological advancements is the use of artificial intelligence (AI) in financial management. AI is no longer just a buzzword—it’s actively shaping how we handle money.

- Personalized Advice: AI-powered apps analyze spending patterns and suggest tailored savings or investment strategies.

- Fraud Detection: AI flags unusual transactions instantly, protecting users from scams.

- Chatbots: Virtual assistants provide round-the-clock support for banking or financial questions.

AI doesn’t just make managing money easier; it makes it smarter, adapting to your financial behavior and goals.

Security and Data Protection

With the rise of digital finance comes concerns about security. Cybersecurity is a key factor in personal finance technology. Banks, apps, and platforms implement advanced measures like:

- Encryption: Protecting sensitive financial data during transactions.

- Two-Factor Authentication: Adding extra layers of login security.

- Biometric Verification: Using fingerprints or facial recognition for access.

While technology improves convenience, it also demands that users practice good habits—like avoiding weak passwords and being cautious with public Wi-Fi.

Advantages of Technology in Personal Finance

The role of technology in personal finance is overwhelmingly positive. Some of the key benefits include:

- Convenience: Manage all aspects of money without visiting a physical bank.

- Transparency: Real-time insights into income, spending, and investments.

- Accessibility: Financial tools for all, regardless of income or background.

- Automation: Savings and investments grow with minimal effort.

- Motivation: Gamification and progress tracking encourage better habits.

Challenges and Drawbacks

Despite the advantages, technology in finance isn’t without its challenges.

- Overreliance: People may become too dependent on apps and lose touch with basic money management skills.

- Privacy Concerns: Sharing sensitive data with multiple apps carries risks.

- Impulse Spending: The ease of digital payments can encourage poor habits.

- Learning Curve: Some tools can feel overwhelming to beginners.

Balancing technology with financial discipline is key to long-term success.

The Future of Technology in Personal Finance

The future promises even more innovation in personal finance management. Emerging trends include:

- Blockchain and Cryptocurrencies: More secure, decentralized transactions.

- Voice-Activated Finance: Smart speakers helping manage budgets or pay bills.

- Hyper-Personalization: Financial advice tailored to your lifestyle in real time.

- AI-Driven Forecasting: Predictive models that help you prepare for financial events.

As technology continues to evolve, personal finance management will only become more efficient and integrated into daily life.

Practical Tips for Using Technology Wisely

- Start Small: Begin with one budgeting app before branching into multiple tools.

- Set Boundaries: Use alerts to avoid overspending on digital payments.

- Prioritize Security: Enable two-factor authentication and use strong passwords.

- Stay Educated: Learn how tools work instead of relying blindly on automation.

- Review Regularly: Technology is a tool, but you still need to check your finances periodically.

Conclusion

Technology has transformed the way we manage money, putting powerful tools into the hands of everyday people. Whether it’s budgeting apps, investment platforms, or AI-driven insights, digital innovations help us make smarter, faster, and more informed financial decisions.

But technology is not a replacement for responsibility. True financial success comes from combining these tools with good habits, discipline, and clear goals. Used wisely, technology can help you take control of your finances, build wealth, and create the financial future you want.

Also visit:-

10 Simple Ways to Bring Romance Back into Your Marriage

FAQs on The Role of Technology in Personal Finance Management

1. What is personal finance management?

Personal finance management refers to the process of budgeting, saving, investing, and monitoring income and expenses to achieve financial goals.

2. How has technology changed personal finance?

Technology has made managing money easier, faster, and more transparent by providing tools like budgeting apps, mobile banking, and investment platforms.

3. What are the best tools for managing personal finances?

Popular tools include budgeting apps like Mint, YNAB, and PocketGuard, as well as digital banks and investment apps.

4. Is online banking safe for managing finances?

Yes, most banks use encryption, two-factor authentication, and fraud detection to ensure security, though users must also follow safe practices.

5. What is the role of mobile banking in personal finance?

Mobile banking provides instant access to accounts, enables bill payments, transfers, and helps track spending in real time.

6. How do budgeting apps help with money management?

They automatically categorize spending, set savings goals, and offer alerts to prevent overspending.

7. Can digital payment platforms improve financial management?

Yes, apps like PayPal, Venmo, and Google Pay make payments faster and provide digital records for easier tracking.

8. What are robo-advisors in investing?

Robo-advisors are automated platforms that use algorithms to create and manage investment portfolios based on your goals.

9. Do I need financial knowledge to use investment apps?

Not necessarily. Many apps provide educational resources, while robo-advisors handle investing decisions automatically.

10. Can technology help reduce debt?

Yes, debt management apps create payoff strategies, track progress, and send reminders to stay on track.

11. How does technology help with credit monitoring?

Credit monitoring apps provide free credit scores, reports, and alerts for suspicious activity.

12. What role does AI play in personal finance?

AI analyzes spending patterns, predicts future expenses, offers tailored advice, and detects fraudulent transactions.

13. Are AI-powered finance apps reliable?

Most are reliable, but they should be used alongside personal judgment and regular reviews of financial activity.

14. How can I keep my financial data safe online?

Use strong passwords, enable two-factor authentication, avoid public Wi-Fi for banking, and update apps regularly.

15. Can technology help me save money?

Yes, through automation, round-up savings features, and tools that allocate funds directly into savings accounts.

16. What are the benefits of personal finance apps?

They improve awareness, track progress toward goals, and encourage disciplined financial behavior.

17. Do budgeting apps cost money?

Some are free with basic features, while others charge subscription fees for advanced tools.

18. Can I manage all my finances with one app?

Some all-in-one apps exist, but often you’ll use a combination of budgeting, investment, and banking apps for full coverage.

19. Are digital payments better than cash for budgeting?

Digital payments provide a clear record of spending, but they may also encourage impulse spending if not managed carefully.

20. What is a digital wallet?

A digital wallet is a mobile app or device feature that stores payment information securely for quick transactions.

21. Can kids or teens use finance apps?

Yes, some apps are designed for young users, teaching them money management skills with parental oversight.

22. How do I choose the best finance app for me?

Consider your goals—budgeting, saving, investing, or debt management—and choose apps with features that match.

23. Does technology replace financial advisors?

Not completely. Technology simplifies many tasks, but human advisors can still provide personalized advice for complex financial situations.

24. How often should I check my finance apps?

Weekly reviews are ideal, but daily quick checks can help you stay aware of your spending habits.

25. Can I use multiple finance apps together?

Yes, many apps sync with each other and with your bank accounts for seamless financial management.

26. What’s the biggest risk of using finance technology?

The main risks include data breaches, privacy concerns, and overreliance on automation.

27. Can finance apps help with retirement planning?

Yes, many apps calculate savings needs, project retirement funds, and suggest investment strategies.

28. What are some examples of AI in finance apps?

AI chatbots, personalized recommendations, fraud alerts, and predictive analytics are common examples.

29. How does technology encourage financial discipline?

Through reminders, spending alerts, savings milestones, and gamification features that reward progress.

30. Can technology prevent overspending?

Yes, by setting budgets, sending alerts when you’re close to limits, and tracking daily spending.

31. Do I need a strong internet connection for finance apps?

Yes, since most apps rely on real-time data, a stable connection ensures smooth use.

32. How do finance apps make money?

Through subscription fees, premium features, affiliate partnerships, or financial product recommendations.

33. Can I use finance technology internationally?

Yes, though availability of apps and banking features may vary by country.

34. Are cryptocurrency wallets part of personal finance technology?

Yes, crypto wallets are becoming part of broader personal finance management for those investing in digital assets.

35. Is personal finance technology suitable for beginners?

Absolutely. Most apps are designed to be user-friendly and educational for first-time users.

36. Can voice assistants manage finances?

Yes, some smart speakers can check balances, pay bills, or track expenses through linked apps.

37. How does blockchain impact personal finance?

Blockchain offers secure, transparent, and decentralized ways of handling transactions and investments.

38. Should I rely only on apps for financial planning?

No. Apps are powerful tools, but combining them with financial literacy and manual reviews ensures better results.

39. What are the future trends in personal finance technology?

Expect more AI-driven personalization, blockchain adoption, voice-activated services, and deeper integration with daily life.

40. How do I get started with technology-based financial management?

Start by downloading a budgeting app, linking your accounts, and tracking expenses. From there, explore savings and investment apps to grow your wealth.

Would you like me to now also write the rich snippets structured data (schema markup) in one script (organization + article + breadcrumb + FAQ) like I’ve done for your previous finance posts?

Also visit:-